Public Mobile Gaming Publishers: Resilience & Adaptation in a Shifting Landscape

Written by our Partner, InvestGame.

Survival Strategies, Market Trends, and the Path Forward

The mobile gaming market remains one of the largest segments in interactive entertainment, with in-app purchases (IAP) generating ~$60B in 2024. However, the mobile gaming industry has undergone a significant transformation over the past five years, shifting from a high-growth expansion to a mature market characterized by operational efficiency, financial discipline, and single-digit growth.

During the 2020–2021 boom, mobile gaming saw record-high UA spending, valuation surges, and aggressive M&A activity. Between 2020 and 2022, mobile gaming accounted for over 60% of all gaming M&A transactions’ value, with major deals such as Zynga’s $12.7B acquisition by Take-Two and Scopely’s $4.9B sale to Savvy Games Group. Even in Q4’24, mobile remained at the center of industry consolidation, with three of the four largest M&A deals involving mobile gaming assets.

The momentum has continued into 2025, with Dream Games planning to secure one of the biggest-ever $2.5B gaming funding rounds, signaling ongoing investor interest in high-performing mobile studios. Meanwhile, Niantic’s $3.5B sale of its gaming division to Scopely suggests that further consolidation may be on the horizon.

However, despite these headline deals, the broader mobile gaming market landscape has changed. Post-pandemic normalization, Apple’s IDFA changes, and rising UA costs have forced companies to rethink their strategies—the once M&A-heavy growth model has given way to profitability-oriented restructurings, team layoffs, and strategic reviews.

We’ll dive into how Western publicly listed mobile gaming publishers Playtika, Stillfront, Modern Times Group, GDEV, and Playstudios are tackling the shifting landscape. Each brings a unique angle to their gaming portfolios—from social casino and casual to mid-core segments—and distinct strategic approaches. We’ll explore how they’re adapting to the new market realities by addressing five key questions:

- What are the main financial trends among mobile gaming companies?

- How have operational metrics evolved over time?

- How have market capitalization and share price dynamics reflected these shifts?

- What strategies have companies implemented to optimize their business?

For a detailed analysis, check out the accompanying report:

GDEV x InvestGame — Feature #9

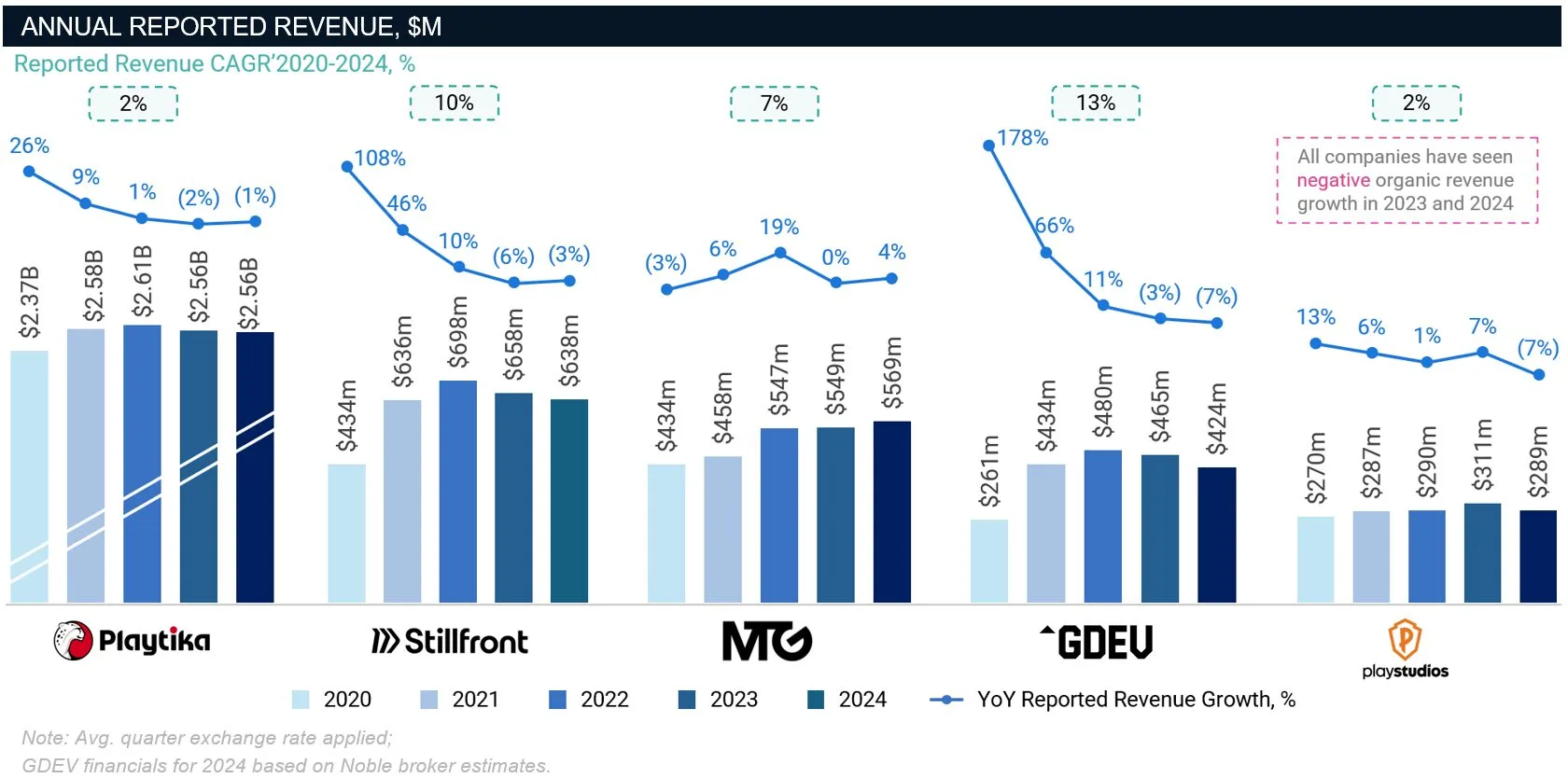

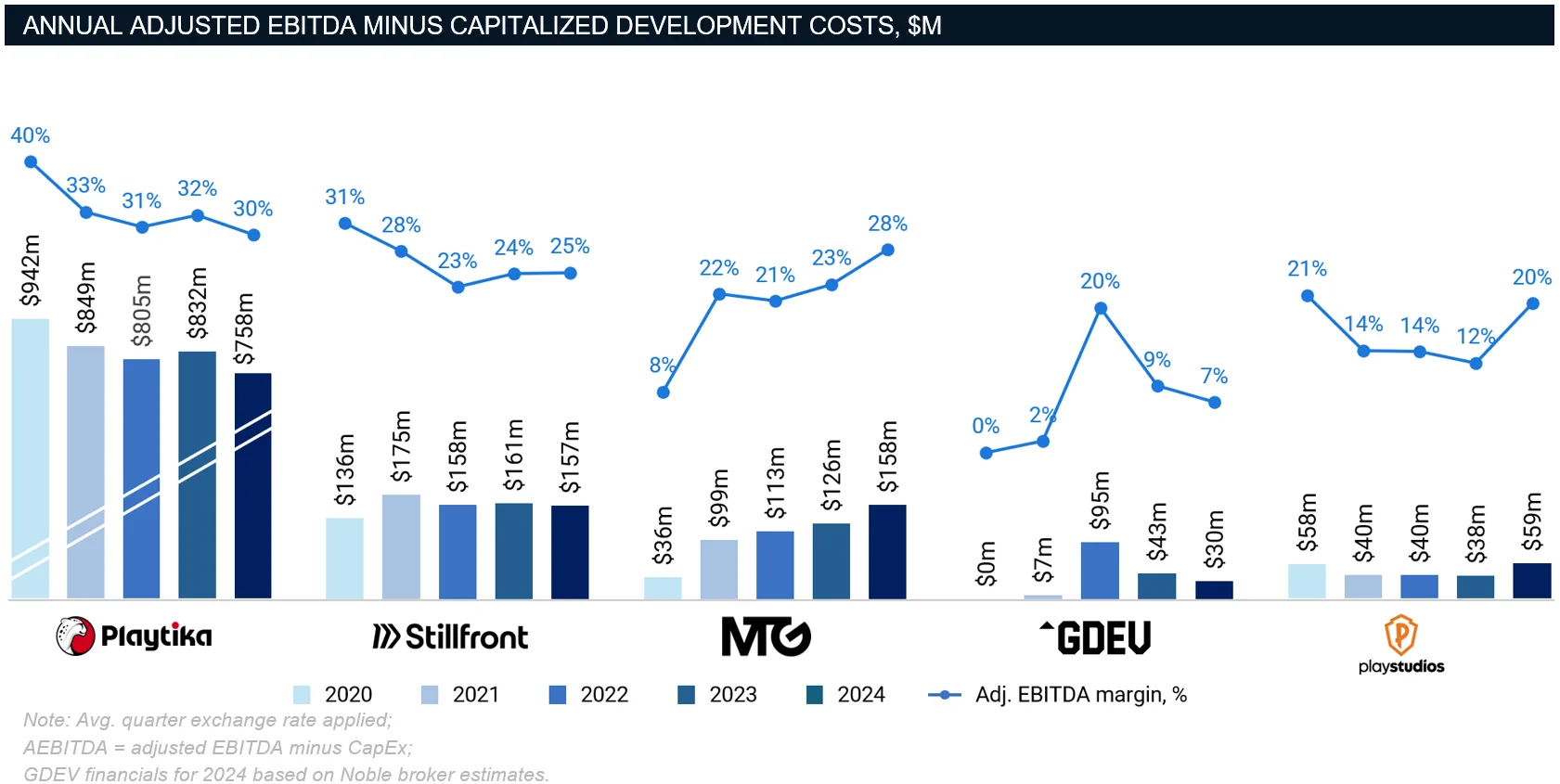

After years of aggressive expansion fueled by acquisitions and UA spending, mobile gaming companies faced a harsh financial reset in 2022–2023. As user acquisition became more expensive and engagement trends shifted after the pandemic boom, revenue growth slowed or even turned negative. Even companies that maintained positive Revenue CAGRs (mainly in the single-digit range) experienced squeezed profitability, as rising costs eroded EBITDA margins.

To adapt, Playtika has intensified its focus on casual gaming, as its social casino segment has faced challenges. The company is also advancing its Direct-to-Consumer (DTC) monetization strategy to reduce reliance on platform fees and improve profit margins. Stillfront, once one of the most aggressive acquirers, halted its M&A spree, shifting to cost-cutting and focusing on operational efficiency.

Meanwhile, MTG proved that M&A could still be effective—if executed properly. The company’s disciplined acquisition strategy, particularly with PlaySimple and Snowprint studios, helped it achieve strong Q4’24 results with 9% organic growth and record profits despite broader industry challenges.

GDEV and Playstudios shifted their focus from expansion to stability. After a temporary trading halt, GDEV concentrated on UA optimization and platform diversification (Steam) to hedge against mobile volatility. Playstudios, on the other hand, leaned into loyalty-based engagement (playAWARDS), proving that retention-focused monetization could sustain revenue without aggressive UA reinvestment.

With cheap growth no longer an option, companies have fundamentally restructured their strategies. The new focus is profitability, player retention, and efficiency rather than rapid expansion.

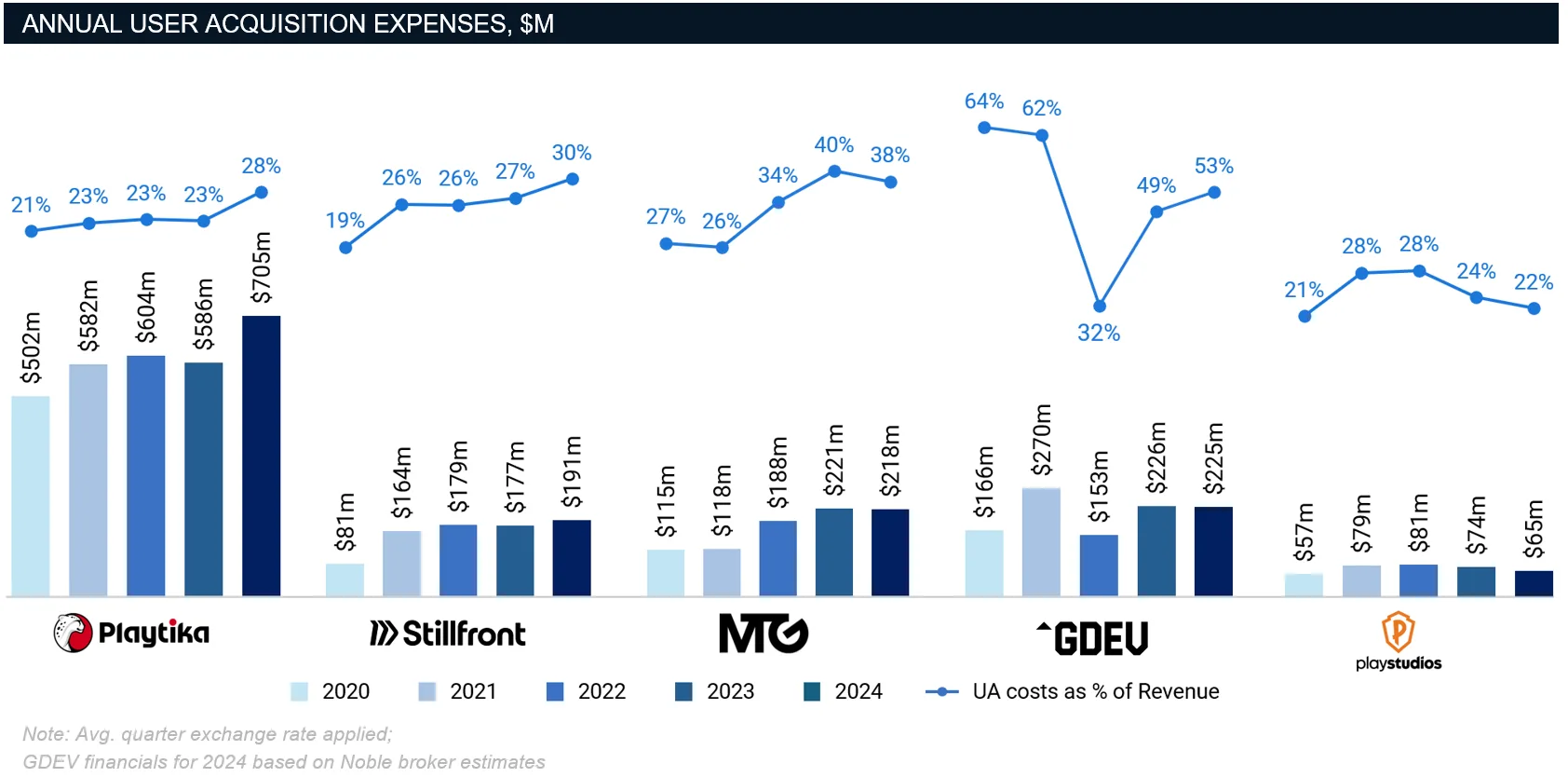

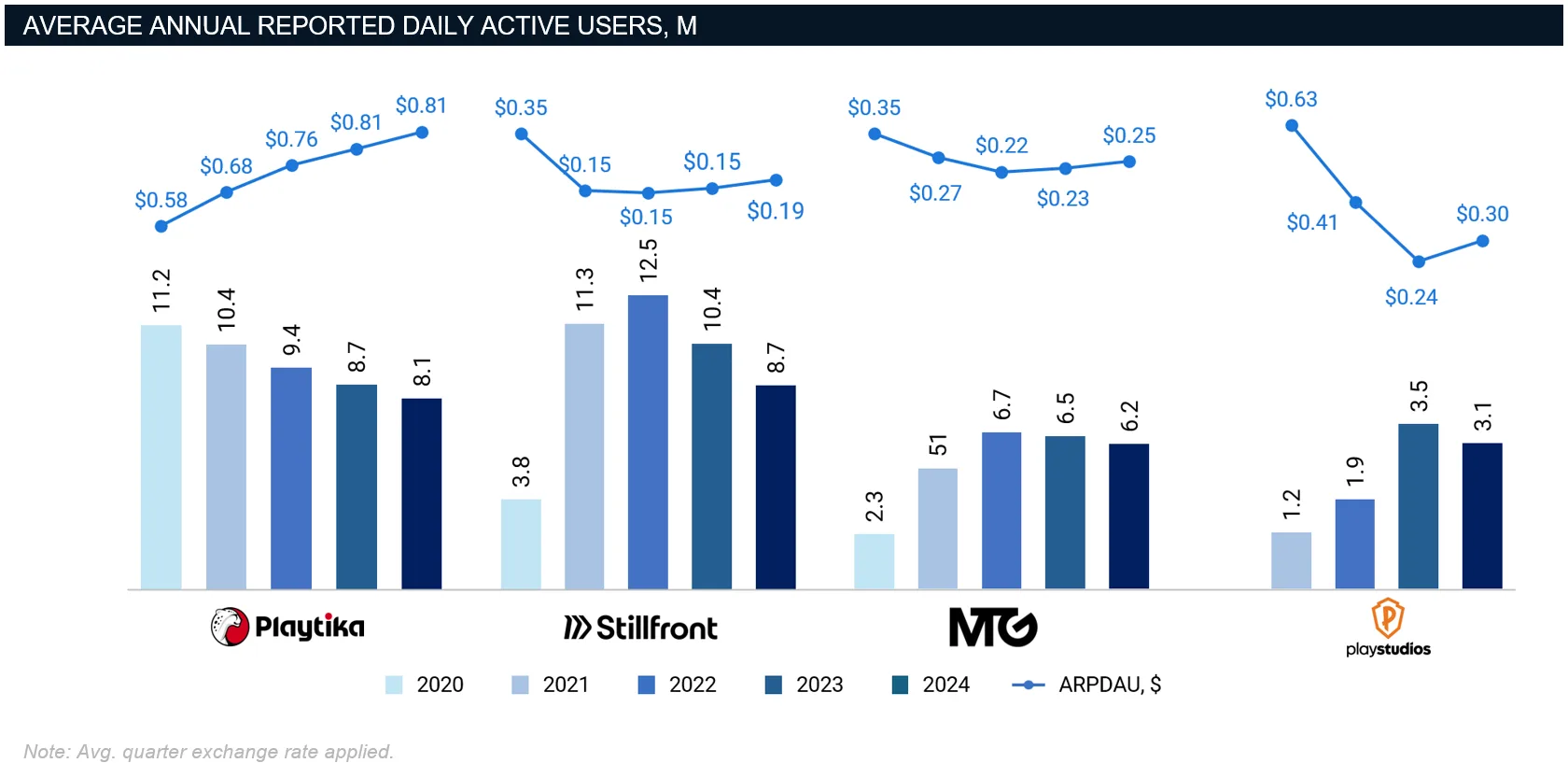

User acquisition reckoning: the playbook has changed

For years, user acquisition (UA) was the primary driver of growth, with companies often spending up to half their revenue on paid installs. By 2023, however, it became clear that high UA spending no longer guaranteed stable financial performance amid the changing playbook

Three major factors drove this shift:

- IDFA changes have made it more challenging for advertisers to track user behavior across apps. This change has led to decreased ad targeting and attribution accuracy, resulting in increased costs for acquiring new users.

- Post-pandemic player engagement decline leading to changes in player behavior and taking time for publishers to adapt to new cohort performance realities (i.e., retention and monetization), leading to more cautious UA budgets.

- The mobile gaming market saturation intensifies competition for user attention and leads to diminishing returns from traditional performance marketing efforts.

Survival Strategies: How Have Companies Adjusted?

To navigate the challenges, the industry has moved beyond pure UA scaling by shifting focus toward player retention and LTV growth, with each company taking a different approach:

- Some mobile publishers invested in first-party data, LiveOps capabilities, and community-driven / loyalty engagement to increase ARPPU and retain users for longer as it’s more cost-effective vs. acquiring new ones;

- Others diversified into PC / cross-platform gaming and brand partnerships, aiming to acquire players at lower costs through other channels (e.g., web, Steam) and potentially bringing a more engaged user base.

- Hybrid monetization models emerged to drive a more sustainable and predictable revenue stream.

These shifts highlight a broader industry trend—from relying heavily on acquisitions toward building more substantial in-house capabilities and prioritizing efficiency and organic growth.

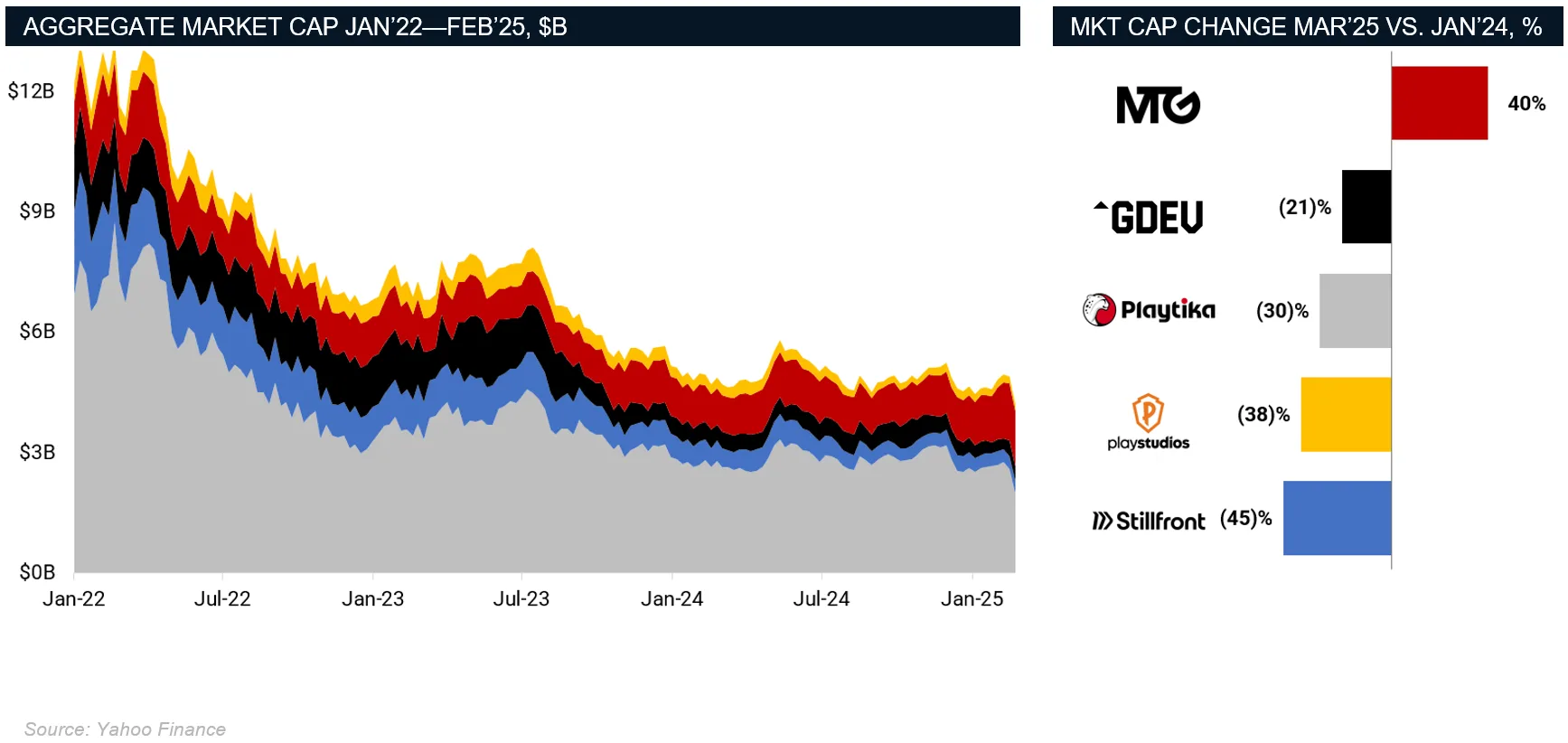

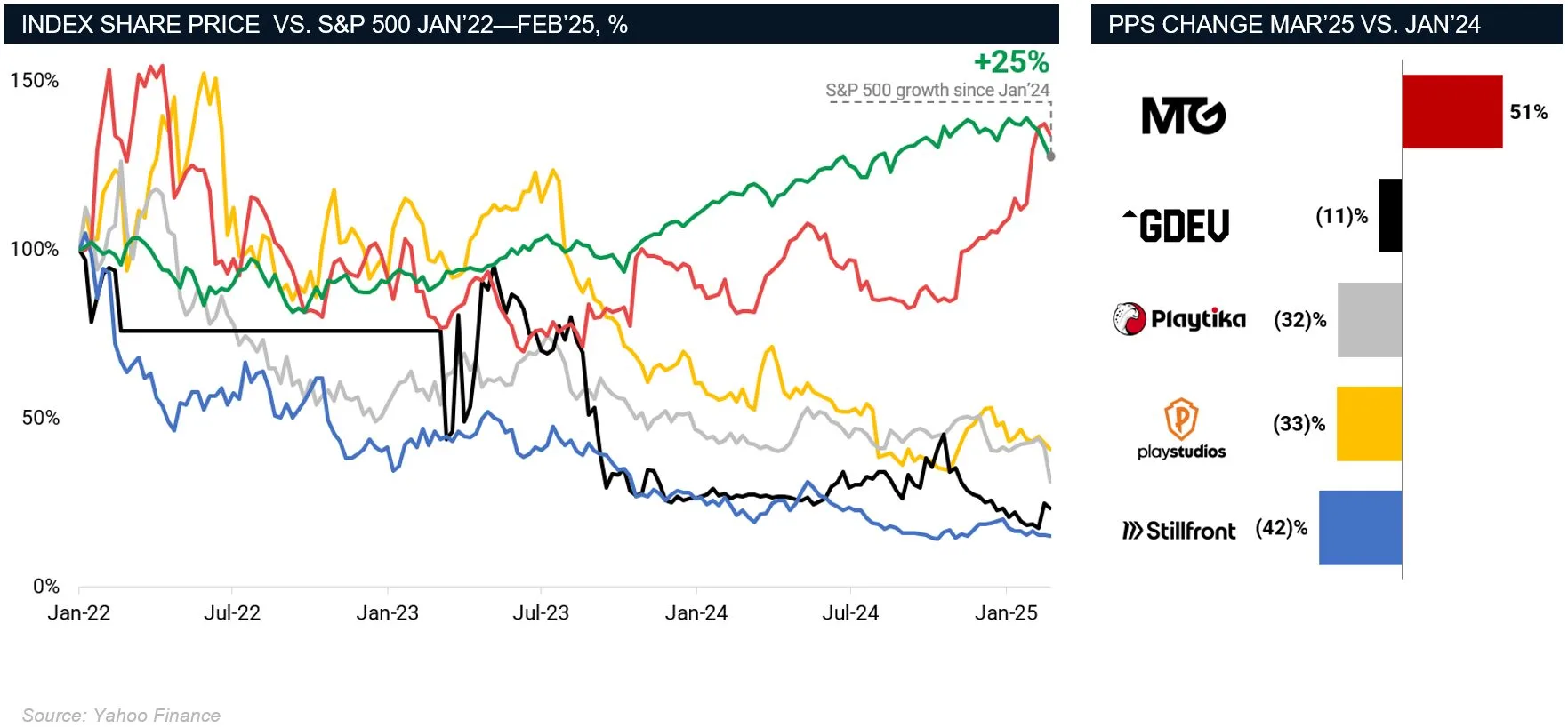

Market capitalization: Investor sentiment turns cautious

Public stock performance closely tracked broader mobile industry trends, with many publishers outperforming the overall market growth between 2020 and 2022. However, as the industry shifted to the new reality described above, market valuations rapidly declined—market caps have shrunk by more than half since Jan’22. This decline reflects weaker operational performance by mobile studios and a significant shift in investor sentiment.

Since early 2024, only MTG has recovered substantially, posting a 40% increase in market cap and share price, nearly returning to Jan’22 levels. Investors have rewarded MTG’s successful M&A integrations, organic revenue growth, and improved EBITDA margins.

Below are key trends shaping valuations over recent years:

- Companies overly reliant on M&A without demonstrating clear organic growth post-acquisition experienced significant stock declines, as integration efforts and expected synergies often fell short of investor expectations.

- Studios prioritizing growth at all costs faced increasing profitability concerns due to declining user acquisition efficiency and rising OpEx (i.e, headcounts). Investor preferences shifted notably from revenue growth “at all costs” to profitable scalability.

- Studios that optimized existing assets and maintained financial discipline (i.e., healthy EBITDA margins) performed comparatively better, demonstrating more stable share price performance.

Conclusion: What’s next for mobile gaming?

The mobile gaming industry is entering a new era—one defined not by rapid expansion but by sustainable, profitability-first strategies.

After years of M&A-driven growth and UA-heavy marketing models, companies are now adapting to a reality where financial discipline, retention-based monetization, and cross-platform expansion are the key priorities.

Studios that effectively balance strategic acquisitions with operational efficiency and organic user engagement will shape the industry’s future. In contrast, studios overly reliant on costly UA campaigns or lacking a thoughtful M&A strategy will likely continue to experience valuation turbulence.

In this evolving market, the winners will not be those who grow the fastest in the short term but those who adopt a strategic, long-term focus and grow intelligently.